Building A Core Allocation To Private Markets

For decades, portfolio construction rested on a simple foundation.

For decades, portfolio construction rested on a simple foundation. Public equities delivered growth, while bonds provided income and stability. The 60/40 portfolio became the default framework for long-term wealth.

That world has changed. A growing share of economic activity now sits outside public markets.

Companies are staying private for longer, banks are providing less balance sheet lending, and investment in infrastructure and essential services increasingly occurs away from listed markets.[1]

At the same time, public markets have become more concentrated, and the diversification between equities and bonds has proven less reliable.

Traditional portfolios no longer capture the full opportunity set available across the broader global economy.

For investors seeking growth, income and resilience, the question is not whether to allocate to private markets, but how to do so in a disciplined and enduring way.

This can be understood through four complementary private market engines.

Four Complementary Private Market Engines

Private markets are not a single exposure, but a set of complementary return engines that operate across a global opportunity set and work together within a total portfolio.

Together, these strategies provide exposure to different components of the real economy: ownership, financing, essential assets and portfolio optimisation.

Private Equity drives long-term capital growth through active ownership and operational improvement.

Private Credit provides contractual income through senior secured lending and junior capital solutions, with disciplined underwriting.

Infrastructure offers exposure to essential assets with durable, often inflation-linked cash flows.

Secondaries provide access to more mature portfolios, offering greater visibility on underlying performance and reduced blind pool risk.

Individually, each strategy has merit. Allocating to one alone may emphasise a single objective, but it leaves the portfolio exposed to a single return driver.

Combined, they create a diversified allocation aligned to growth, income and resilience.

Europe: A Standout Opportunity Within a Global Market

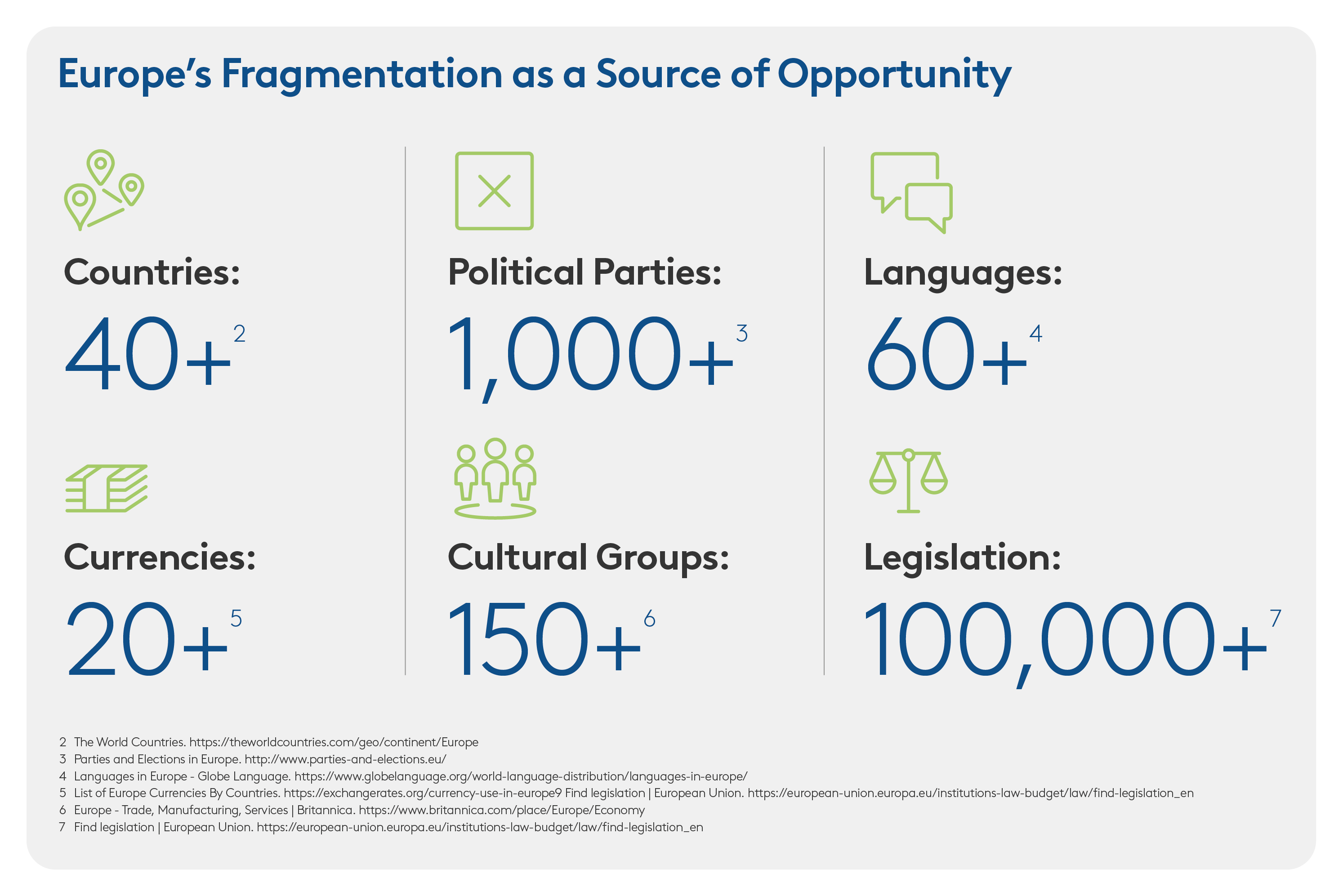

These complementary engines can be especially powerful in more fragmented markets such as Europe.

Europe sits at the centre of several long-term structural shifts. Reindustrialisation, energy transition and strategic autonomy are reshaping the region’s economic landscape.

These transitions are capital intensive, requiring patient ownership, flexible financing and operational expertise. These characteristics are more naturally aligned with private capital than public markets.

At the same time, Europe remains highly fragmented. This creates a local, relationship-driven investment landscape where access is uneven, and where fragmentation itself becomes a source of edge, helping managers with deep local networks and experience to source more proprietary opportunities.

In this environment, coordinated access across private equity, credit, infrastructure and secondaries is not simply a convenience, but a structural advantage.

A Structural Allocation in a Total Portfolio

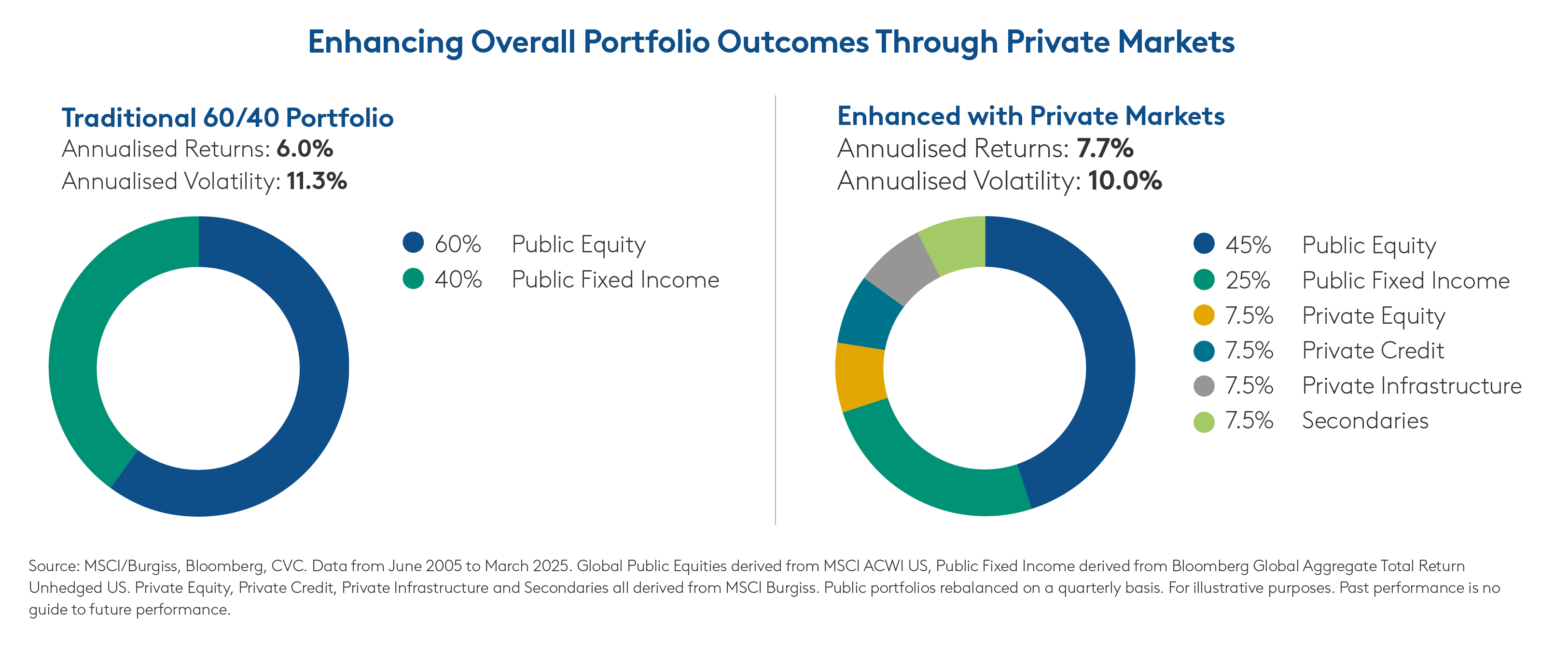

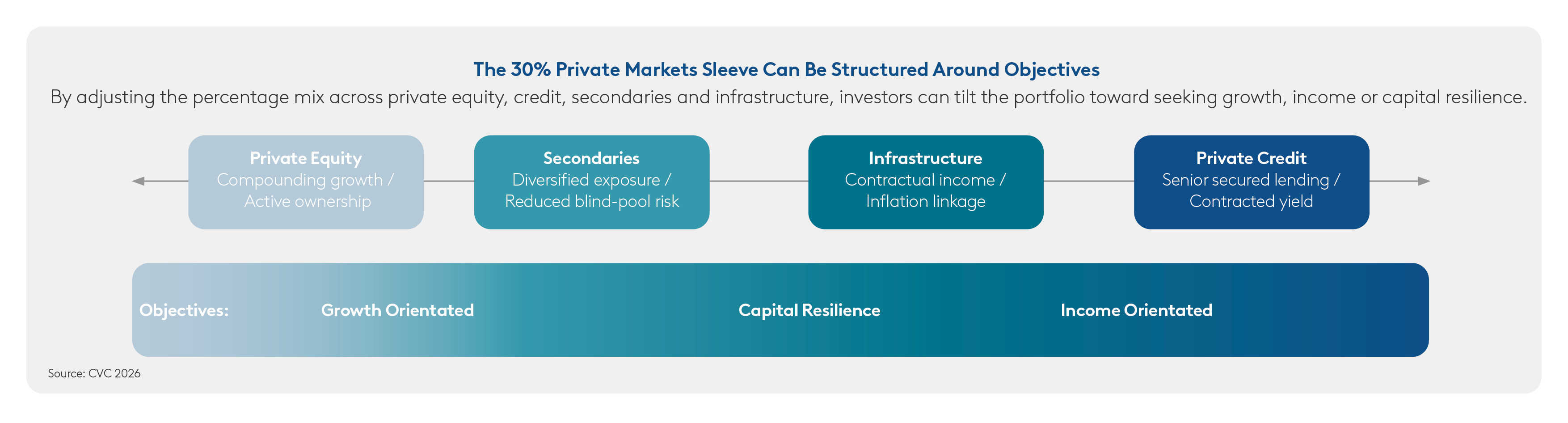

For illustrative purposes, consider a portfolio with a persistent 30% allocation to private markets, alongside public equities and fixed income.

Within that allocation, investors can calibrate exposures to reflect their objectives.

Greater weight to private equity may support growth through capital appreciation and operational value creation.

Increased allocation to private credit and infrastructure may enhance income and resilience through contractual cash flows and senior positioning.

Secondaries can further support resilience and growth by providing exposure to more mature assets, offering greater visibility on underlying performance and contributing to a smoother return profile.

Bringing these strategies together creates a diversified set of return drivers and allows capital to be deployed dynamically across market conditions.

To implement this effectively, an integrated investment platform is not just helpful, it can be a structural advantage, particularly in accessing and executing on opportunities in more fragmented markets such as Europe.

When relationships, deal dynamics and insights are shared across private equity, credit, infrastructure and secondaries teams, sourcing deepens, underwriting strengthens, and opportunity sets expand. This enables more informed and consistent investment decisions.

This level of coordination can be difficult to replicate through separate managers, where fragmented approaches may lead to less consistent outcomes.

Crucially, it enables more deliberate and effective portfolio construction, combining growth, income and resilience in a single framework.

Portfolio Implications

The traditional portfolio framework is evolving. A changing economic landscape and expanding opportunity set are making private markets an increasingly core part of long-term portfolios.

Within private markets, outcomes are driven by sourcing capability, underwriting discipline and operational expertise, particularly in fragmented markets such as Europe. Manager selection is therefore a key determinant of long-term results.

A consistent allocation across private equity, credit, infrastructure and secondaries provides a foundation to:

- Enhance long-term growth

- Generate diversified income

- Strengthen resilience across economic cycles

This foundation enables investors to calibrate exposure to growth, income and resilience with greater precision, aligning portfolios more closely with investment objectives.

Rather than building exposure strategy by strategy, allocating across these capabilities within a coordinated, multi-engine framework offers a more integrated and adaptable approach to long-term wealth creation.

DISCLAIMER:

Nothing in this publication constitutes a valuation or investment judgment regarding any specific financial instrument, issuer, security, or sector mentioned or referenced herein. The content presented does not represent a formal or official view of CVC and is not intended to relate specifically to any investment strategy, vehicle, or product offered by CVC. This publication is provided solely for informational purposes and is intended to serve as a conceptual framework to support investors in conducting their own analysis and forming their own views on the subject matter discussed. No assurance can be given that any investment strategy discussed will be successful. Past market trends are not reliable indicators of future performance, and actual outcomes may vary significantly. The information, including any commentary on financial markets, is based on current market conditions, which are subject to change and may be superseded by subsequent events. THIS CONFIDENTIAL DOCUMENT IS NOT INTENDED TO FORM THE BASIS OF ANY INVESTMENT DECISION AND MAY NOT BE USED FOR AND DOES NOT CONSTITUTE AN OFFER TO SELL, OR A SOLICITATION OF ANY OFFER TO SUBSCRIBE FOR OR PURCHASE ANY INTERESTS OR TO ENGAGE IN ANY OTHER TRANSACTION. Nothing contained herein shall be deemed to be binding against, or to create any obligations or commitment on the part of, the addressee nor any of CVC Capital Partners plc, Clear Vision Capital Fund SICAV-FIS S.A, each of their respective successors or assigns and any form of entity which is controlled by, or under common control with CVC Capital Partners plc or Clear Vision Capital Fund SICAV-FIS S.A. (from time to time the “CVC Entities“ or “CVC” and each a “CVC Entity”). For the purpose of the foregoing definitions, control includes the power to (directly or indirectly and whether alone or with others) appoint or remove a majority of an entity’s directors or its general partner, manager, adviser, trustee, founder, guardian, beneficiary or other management officeholder) and controlled and controlling shall be interpreted accordingly. No CVC Entity undertakes to provide the addressee with access to any additional information or to update this Confidential Document or to correct any inaccuracies herein which may become apparent. Certain information contained herein (including certain forward-looking statements, financial, economic and market information) has been obtained from a number of published and non-published sources prepared by other parties and companies, which may not have been verified and in certain cases has not been updated through the date hereof. While such information from other parties and companies is believed to be reliable for the purpose used herein, no member of CVC, any of their respective affiliates or any of their respective directors, officers, employees, members, partners or shareholders assumes any responsibility for the accuracy or completeness of such information. Certain economic, financial, market and other data and statistics produced by governmental agencies or other sources set forth herein or upon which the CVC’ analysis and decisions rely may prove inaccurate. Nothing contained herein shall constitute any assurance, representation or warranty and no responsibility or liability is accepted by CVC or its affiliates as to the accuracy or completeness of any information supplied herein or any assumptions on which such information is based. Further, this Confidential Document reflects only the views of CVC with respect to private equity markets and other market participants may hold different views or opinions. Accordingly, each Recipient should conduct their own independent due diligence and not rely on any statement or opinion offered herein. In addition, no responsibility or liability or duty of care is or will be accepted by CVC or its respective affiliates, advisers, directors, employees or agents for updating this Confidential Document (or any additional information), or providing any additional information to you. Accordingly, to the fullest extent possible and subject to applicable law, none of CVC or its affiliates and their respective shareholders, advisers, agents, directors, officers, partners, members and employees shall be liable (save in the case of fraud) for any loss (whether direct, indirect or consequential), damage, cost or expense suffered or incurred by any person as a result of relying on any statement in, or omission from, this Confidential Document.