How Private Equity Secondaries Can Improve Portfolio Outcomes

What Secondaries Are

Instead of investing at the start of a fund or company’s journey, secondaries involve buying into existing private equity investments.

These are assets that have been owned, developed and actively managed, often for several years.

This gives investors exposure to value creation already underway, greater visibility on performance, and the potential to acquire high quality investments at a discount.

What Secondaries Deliver

This translates into a distinct set of portfolio benefits:

- Greater visibility and reduced blind pool risk, with known, more mature assets.

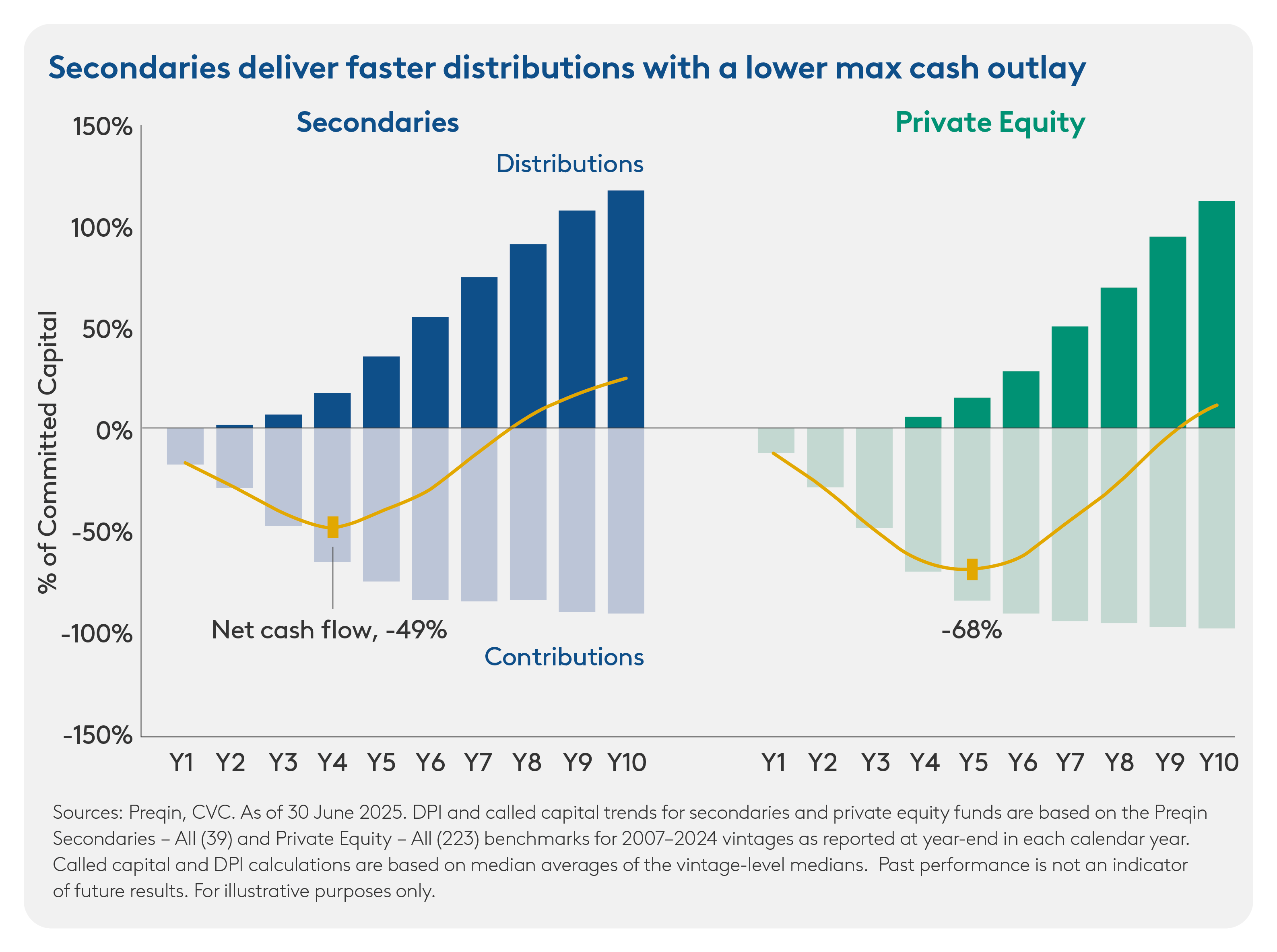

- Faster capital return, with a reduced J-curve effect as investments are closer to exit.

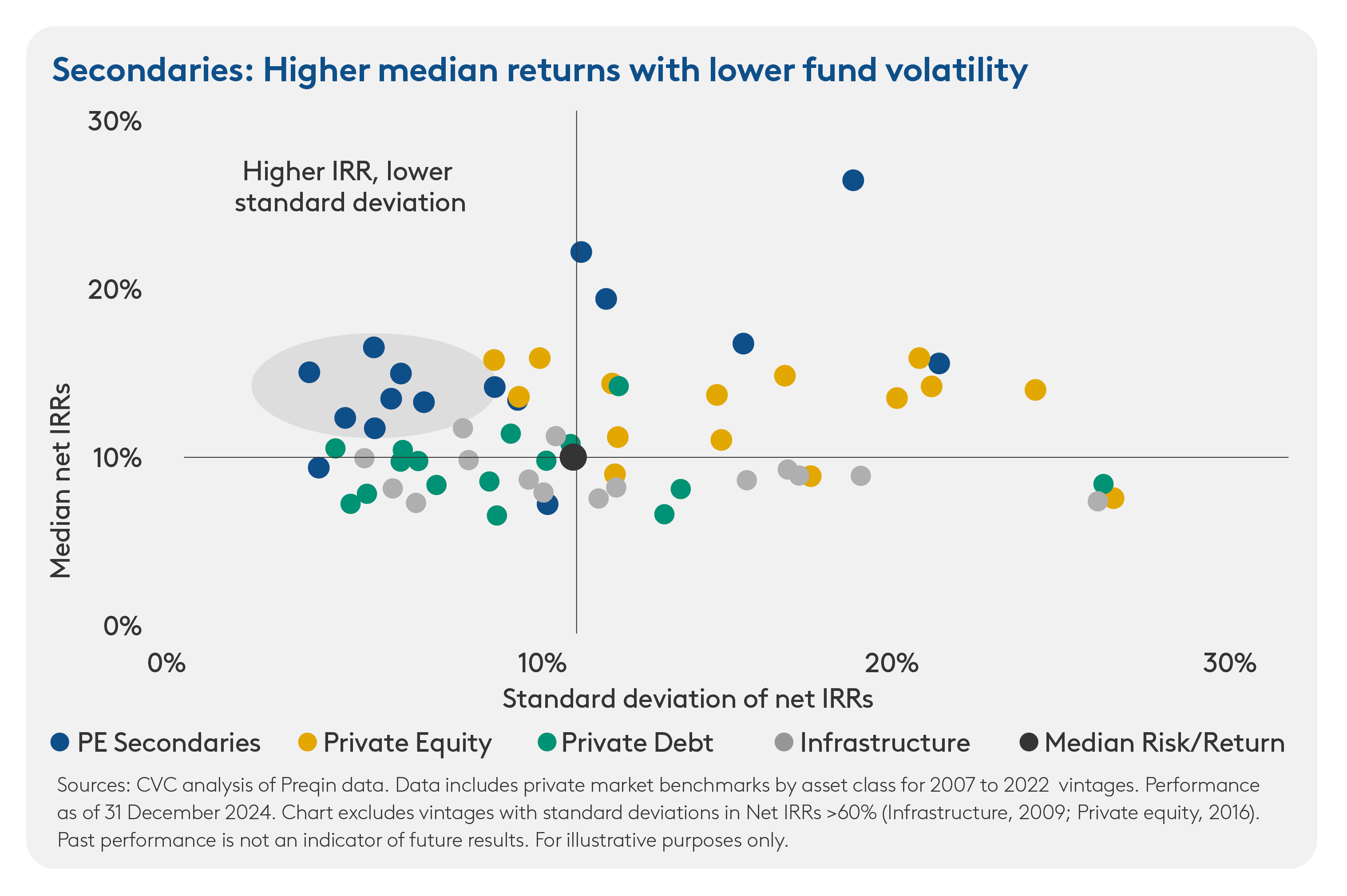

- More consistent return outcomes, supported by diversified and partially de-risked assets.

Secondaries’ Structural Ascent

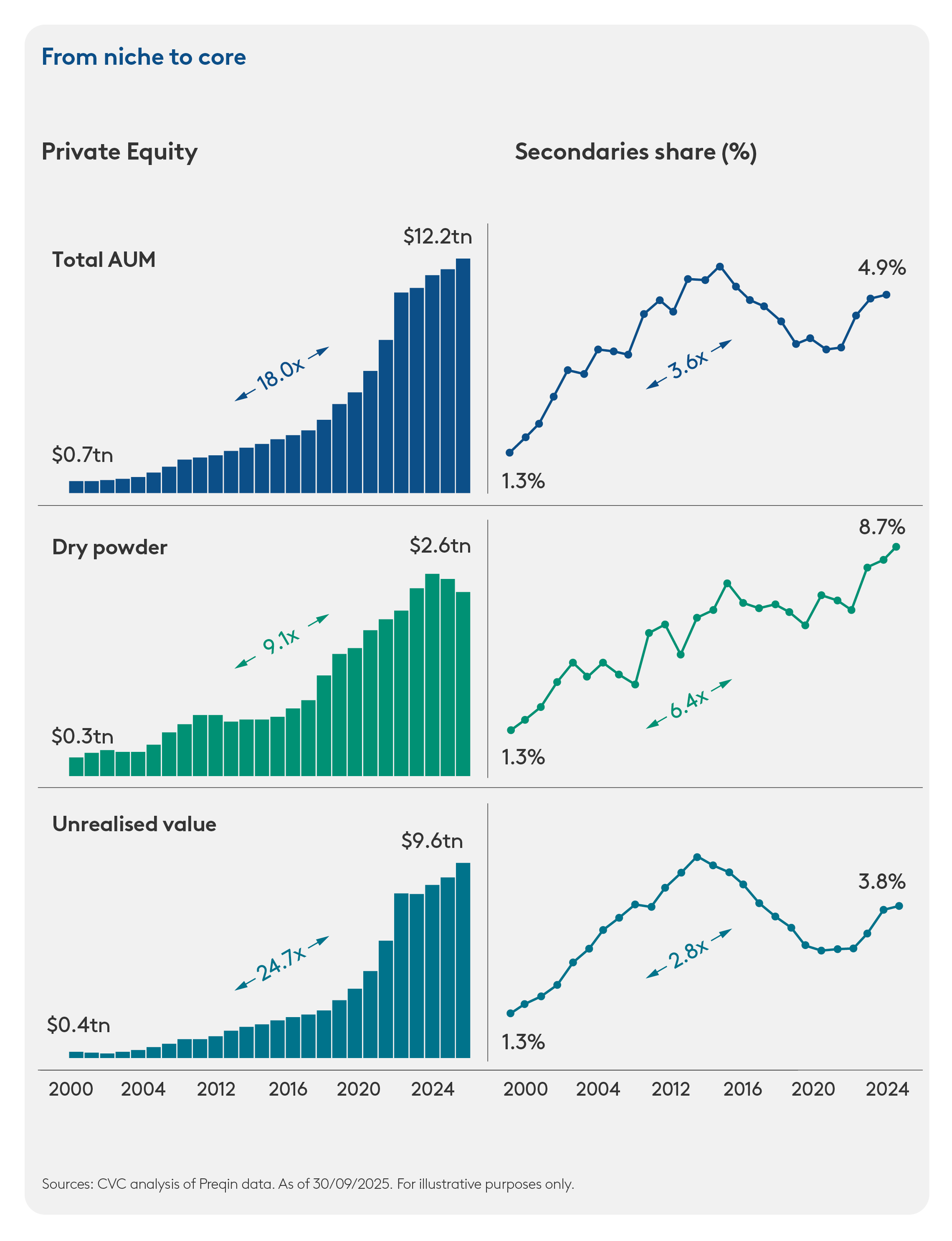

Private equity secondaries have evolved from a niche liquidity solution into a core and rapidly expanding segment of the private markets landscape.

Persistent distribution slowdowns, extended holding periods and significant unrealised value across private equity portfolios have created a growing imbalance between capital invested and capital returned to investors.

Secondaries provide flexibility within an otherwise illiquid asset class, enabling liquidity generation, active portfolio management and strategic repositioning for both Limited Partners (LPs) and General Partners (GPs), while allowing underlying assets additional time to realise value.

These dynamics are driving a broader, deeper and increasingly attractive opportunity set for secondary investors across both LP-led and GP-led transactions.

Where The Opportunity Lies

Secondaries opportunities broadly fall into two categories:

LP-led transactions

These involve buying existing fund interests from investors.

Investors may sell to rebalance portfolios, manage liquidity, or adjust exposures in a changing environment.

These transactions can offer enhanced visibility on underlying portfolio performance and the potential to acquire high-quality assets at attractive entry valuations relative to primary investments.

GP-led transactions

These involve acquiring assets directly from fund managers, often through continuation vehicles.

These are typically high-quality companies that managers know well and believe have further value to realise.

This reflects a broader shift in private equity, where strong assets are held for longer to capture their full potential, rather than being sold according to a predefined fund life.

For investors, this provides access to concentrated, high conviction opportunities in seasoned assets, often alongside leading sponsors.

![]()

Why This Matters For Investors

Across both types of transactions, the common theme is access to seasoned assets.

Companies are already operating, strategies are in place, and value creation is underway.

This can lead to:

- more informed underwriting

- shorter time to liquidity

- and a more balanced risk return profile relative to primary investments

The result is an investment profile that complements traditional private equity, providing access to the same asset class at a different stage of the lifecycle.

Why Manager Selection Is Key

While the opportunity set is large, outcomes can vary significantly.

Secondaries is a sourcing driven market, where access, judgement and discipline determine outcomes.

The most attractive opportunities are often proprietary and require deep relationships with both investors and fund managers.

A leading manager can review a wide universe of transactions but invest selectively, focusing on situations where asset quality, pricing and future value creation align.

Experience is also essential in assessing assets that are already in motion, understanding what has been achieved and what remains to be delivered.

For investors, the key challenge is not whether to allocate to secondaries, but how to access the most attractive opportunities in a consistent and scalable way.

DISCLAIMER:

This confidential document (this “Confidential Document”) is being communicated to a limited number of sophisticated persons (each, a “Recipient”) by CVC, as defined below for information purposes only. THIS CONFIDENTIAL DOCUMENT IS NOT INTENDED TO FORM THE BASIS OF ANY INVESTMENT DECISION AND MAY NOT BE USED FOR AND DOES NOT CONSTITUTE AN OFFER TO SELL, OR A SOLICITATION OF ANY OFFER TO SUBSCRIBE FOR OR PURCHASE ANY INTERESTS OR TO ENGAGE IN ANY OTHER TRANSACTION.

Nothing contained herein shall be deemed to be binding against, or to create any obligations or commitment on the part of, the addressee nor any of CVC Capital Partners plc, Clear Vision Capital Fund SICAV-FIS S.A, each of their respective successors or assigns and any form of entity which is controlled by, or under common control with CVC Capital Partners plc or Clear Vision Capital Fund SICAV-FIS S.A. (from time to time the “CVC Entities“ or “CVC” and each a “CVC Entity”). For the purpose of the foregoing definitions, control includes the power to (directly or indirectly and whether alone or with others) appoint or remove a majority of an entity’s directors or its general partner, manager, adviser, trustee, founder, guardian, beneficiary or other management officeholder) and controlled and controlling shall be interpreted accordingly. No CVC Entity undertakes to provide the addressee with access to any additional information or to update this Confidential Document or to correct any inaccuracies herein which may become apparent. This Confidential Document is not intended for distribution, and shall not be distributed, in any jurisdiction where such distribution would violate applicable securities laws.

Certain information contained herein (including certain forward-looking statements, financial, economic and market information) has been obtained from a number of published and non-published sources prepared by other parties and companies, which may not have been verified and in certain cases has not been updated through the date hereof. While such information from other parties and companies is believed to be reliable for the purpose used herein, no member of CVC, any of their respective affiliates or any of their respective directors, officers, employees, members, partners or shareholders assumes any responsibility for the accuracy or completeness of such information. Certain economic, financial, market and other data and statistics produced by governmental agencies or other sources set forth herein or upon which the CVC’ analysis and decisions rely may prove inaccurate.

Nothing contained herein shall constitute any assurance, representation or warranty and no responsibility or liability is accepted by CVC or its affiliates as to the accuracy or completeness of any information supplied herein or any assumptions on which such information is based. Further, this Confidential Document reflects only the views of CVC with respect to private equity markets and other market participants may hold different views or opinions. Accordingly, each Recipient should conduct their own independent due diligence and not rely on any statement or opinion offered herein.

In addition, no responsibility or liability or duty of care is or will be accepted by CVC or its respective affiliates, advisers, directors, employees or agents for updating this Confidential Document (or any additional information), or providing any additional information to you.

Accordingly, to the fullest extent possible and subject to applicable law, none of CVC or its affiliates and their respective shareholders, advisers, agents, directors, officers, partners, members and employees shall be liable (save in the case of fraud) for any loss (whether direct, indirect or consequential), damage, cost or expense suffered or incurred by any person as a result of relying on any statement in, or omission from, this Confidential Document.