Why Infrastructure’s Mid-Market Can Strengthen Your Portfolio

What Infrastructure Delivers

At its core, infrastructure is simple. It is the physical backbone of everyday life.

It includes energy grids that power cities, transport networks that keep economies moving, fibre networks that connect people and businesses, and utilities that communities rely on.

These are essential, real world assets providing services with consistent, inelastic demand.

That simplicity translates into powerful investment characteristics:

- Long-term contracted revenues

- Embedded inflation linkage

- Lower sensitivity to economic cycles

- Downside protection

The result is predictable, resilient cash flows with diversification benefits and low correlation to traditional asset classes. A valuable combination for enhancing long-term wealth portfolios.

Structural Growth Is Driving Infrastructure

The next phase of infrastructure is being driven by powerful structural forces:

- Decarbonisation - the shift to renewable energy and electrification

- Digitalisation - exponential growth in data, fibre, and connectivity

Critically, governments cannot fund this transition alone, widening a global funding gap (~$15 trillion by 2040)1, that experienced private investors are well positioned to fill.

How Europe Stands Out

Europe combines:

- Clear policy direction around energy transition and digital buildout2

- Ageing infrastructure in need of upgrade3

- High dependence on private capital to bridge the funding gap4

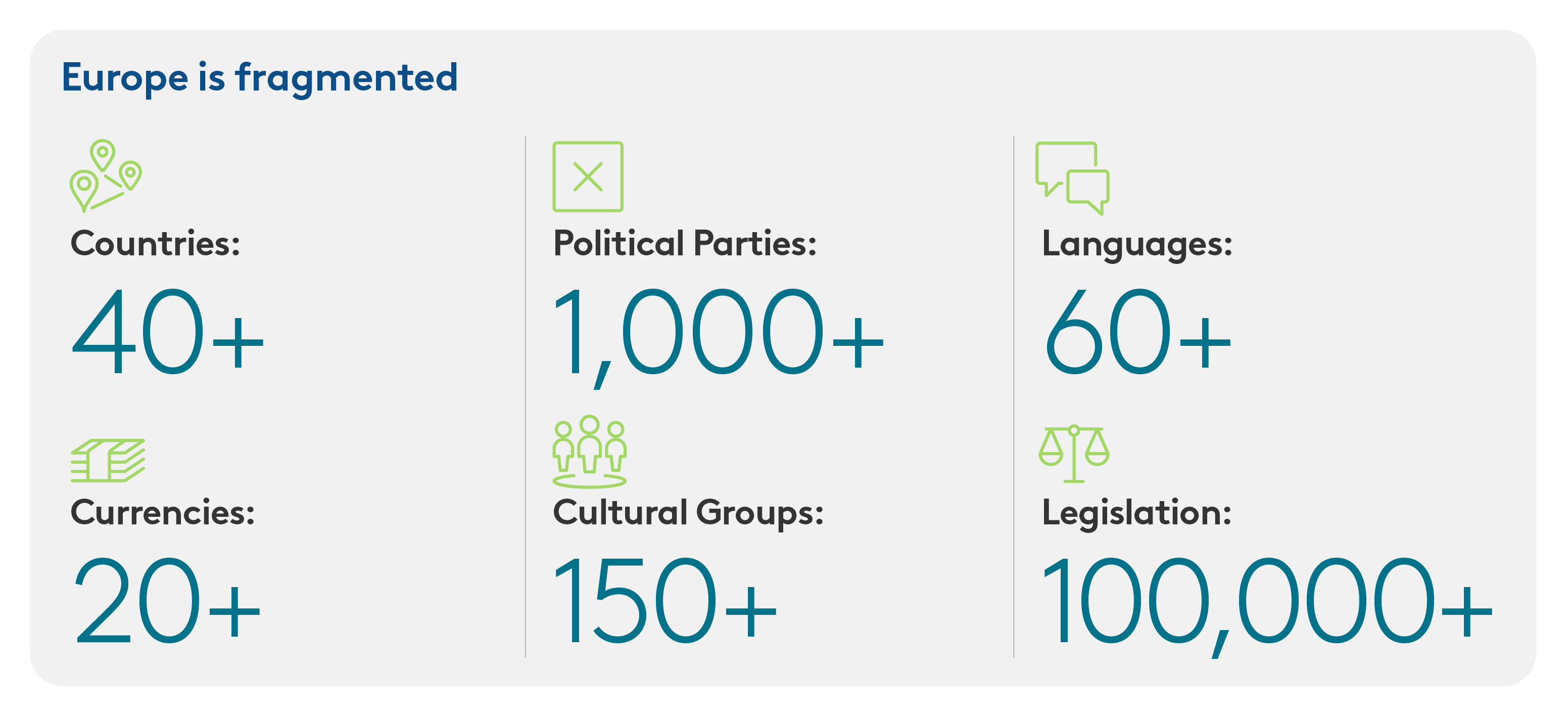

At the same time, Europe is inherently fragmented across countries, languages and regulatory systems.

This fragmentation creates opportunity, but it requires experienced, on-the-ground managers who can leverage deep local insight to source and execute opportunities.

However, not all infrastructure opportunities are equal. The most attractive are increasingly found in the mid-market.

Where The Opportunity Really Lies: The Mid-Market Edge

Some of the most compelling opportunities in infrastructure are not the largest, but in the mid-market, where scale and structural growth intersect.

The mid-market5 represents a large and highly investable universe, accounting for approximately 90% of global infrastructure deal flow.6

The mid-market offers a differentiated investment profile:

- Greater access to proprietary and bilateral transactions

- Typically, lower entry valuations than large-cap assets

- More levers to enhance returns through active value creation

- A wider universe of potential buyers, supporting multiple exit options

- Diversification benefits, as capital has historically concentrated in large-cap infrastructure

Unlike large auctions, the mid-market offers greater scope to create value through active ownership and operational improvement. However, partnering with the right manager is crucial.

Why Manager Selection Is Key

In this environment, access alone is not enough.

Outcomes in infrastructure, particularly in the mid-market, can vary significantly.

Success depends on a manager’s ability to source proprietary opportunities, execute value creation plans and realise investments effectively.

This requires deep local presence, sector expertise and a proven track record across the full investment cycle.

In Europe especially, fragmentation raises the bar. It requires not just capital, but experience on the ground and the ability to operate across complex local markets.

The Bottom Line

Infrastructure remains a cornerstone of resilient portfolios. However, within the asset class, differentiation matters.

The mid-market offers a particularly attractive segment, combining a large investable universe with greater scope for value creation.

Within this, Europe’s mid-market stands out:

- Structural growth, driven by digitalisation and decarbonisation

- Market fragmentation, creating inefficiencies and barriers to entry

- Operational value creation, enabled by active ownership and local expertise

With the right manager, this opportunity can translate into consistent, risk-adjusted returns for long-term investors.

1 Global Infrastructure Outlook. A G20 Initiative. outlook.gihub.org. Retrieved 30 June 2025

2 Massive investment needs to meet EU green and digital targets

3 EU infrastructure modernisation: tackling the finance challenge - GIIA

4 Mind the gap: Europe’s strategic investment needs and how to support them

5 Mid-market = $100m<TEV =<$1bn; large-cap = deals with TEV >$1bn

6 CVC DIF analysis of Preqin data over 10 years to 17 July 2025

DISCLAIMER:

Nothing in this publication constitutes a valuation or investment judgment regarding any specific financial instrument, issuer, security, or sector mentioned or referenced herein. The content presented does not represent a formal or official view of CVC and is not intended to relate specifically to any investment strategy, vehicle, or product offered by CVC. This publication is provided solely for informational purposes and is intended to serve as a conceptual framework to support investors in conducting their own analysis and forming their own views on the subject matter discussed. No assurance can be given that any investment strategy discussed will be successful. Past market trends are not reliable indicators of future performance, and actual outcomes may vary significantly. The information, including any commentary on financial markets, is based on current market conditions, which are subject to change and may be superseded by subsequent events. THIS CONFIDENTIAL DOCUMENT IS NOT INTENDED TO FORM THE BASIS OF ANY INVESTMENT DECISION AND MAY NOT BE USED FOR AND DOES NOT CONSTITUTE AN OFFER TO SELL, OR A SOLICITATION OF ANY OFFER TO SUBSCRIBE FOR OR PURCHASE ANY INTERESTS OR TO ENGAGE IN ANY OTHER TRANSACTION. Nothing contained herein shall be deemed to be binding against, or to create any obligations or commitment on the part of, the addressee nor any of CVC Capital Partners plc, Clear Vision Capital Fund SICAV-FIS S.A, each of their respective successors or assigns and any form of entity which is controlled by, or under common control with CVC Capital Partners plc or Clear Vision Capital Fund SICAV-FIS S.A. (from time to time the “CVC Entities“ or “CVC” and each a “CVC Entity”). For the purpose of the foregoing definitions, control includes the power to (directly or indirectly and whether alone or with others) appoint or remove a majority of an entity’s directors or its general partner, manager, adviser, trustee, founder, guardian, beneficiary or other management officeholder) and controlled and controlling shall be interpreted accordingly. No CVC Entity undertakes to provide the addressee with access to any additional information or to update this Confidential Document or to correct any inaccuracies herein which may become apparent. Certain information contained herein (including certain forward-looking statements, financial, economic and market information) has been obtained from a number of published and non-published sources prepared by other parties and companies, which may not have been verified and in certain cases has not been updated through the date hereof. While such information from other parties and companies is believed to be reliable for the purpose used herein, no member of CVC, any of their respective affiliates or any of their respective directors, officers, employees, members, partners or shareholders assumes any responsibility for the accuracy or completeness of such information. Certain economic, financial, market and other data and statistics produced by governmental agencies or other sources set forth herein or upon which the CVC’ analysis and decisions rely may prove inaccurate. Nothing contained herein shall constitute any assurance, representation or warranty and no responsibility or liability is accepted by CVC or its affiliates as to the accuracy or completeness of any information supplied herein or any assumptions on which such information is based. Further, this Confidential Document reflects only the views of CVC with respect to private equity markets and other market participants may hold different views or opinions. Accordingly, each Recipient should conduct their own independent due diligence and not rely on any statement or opinion offered herein. In addition, no responsibility or liability or duty of care is or will be accepted by CVC or its respective affiliates, advisers, directors, employees or agents for updating this Confidential Document (or any additional information), or providing any additional information to you. Accordingly, to the fullest extent possible and subject to applicable law, none of CVC or its affiliates and their respective shareholders, advisers, agents, directors, officers, partners, members and employees shall be liable (save in the case of fraud) for any loss (whether direct, indirect or consequential), damage, cost or expense suffered or incurred by any person as a result of relying on any statement in, or omission from, this Confidential Document.