Private Equity for Insurers: Unlocking Capital Efficiency under Solvency II

Executive summary

The Solvency II Review may enhance the attractiveness of private equity for European insurers by simplifying the Long-Term Equity Investments (LTEI) framework, under which eligible investments benefit from a Solvency II Capital Requirement (SCR) of 22% vs. 49% + Symmetric Adjustment (SA) for non-LTEI exposures.1 The revised regulations, which are expected to come into force on 30 January 2027, enable a wider range of private equity and infrastructure equity investments to qualify, and position LTEI-eligible assets as increasingly capital-efficient allocations under Solvency II.

Solvency II Review and LTEI

The Solvency II review has reached its final stage, as Commission Delegated Regulation (EU) 2026/2692 entered into force on 10 March,3 and formal application is expected from 30 Jan 2027.

A key component of the reform is the enhancement of the LTEI framework. While LTEI was introduced into Solvency II in 2019, adoption has been limited in practice due to stringent and ambiguous eligibility requirements. The Solvency II Review addresses this by simplifying eligibility criteria and reducing operational constraints, making LTEI a more usable tool for insurers. This aligns with the broader policy objective of enabling insurers to play a greater role in financing the long-term growth of the European economy.

Historically, allocations to private equity have been limited among European insurers - averaging around 2% for European life insurers and 1% for non-life insurers4 - largely due to the “49% + SA” capital requirement applied to unlisted equities under the Solvency II standard formula. In contrast, the LTEI framework allows eligible private equity investments to benefit from a 22% capital requirement, meaningfully reducing the regulatory capital burden and enabling the potential for increased insurer allocation to private equity.

Understanding the LTEI framework:

The Solvency II Review has the potential to enhance the usability of the LTEI framework through the following key changes5:

- Removal of the ring-fencing requirement: Insurers are no longer required to match LTEI portfolios to a ring-fenced set of insurance liabilities, hence reducing operational complexity.

- Relaxed “no forced sale” requirement: The regulation clarifies how this requirement can be demonstrated and allows different methods, subject to supervisory oversight. Insurers now need to demonstrate the ability to avoid forced sales for five years instead of ten years.

- Broader geographic eligibility: Eligible unlisted investments may now be headquartered in EEA or OECD countries, whereas previously eligibility was limited to EEA-only jurisdictions.

- Simplified implementation through fund structures: For collective investment undertakings with a lower risk profile6 - such as unlevered closed-ended AIFs and ELTIFs - eligibility may be assessed at the fund level without a full look-through, potentially making it easier to access LTEI treatment through private equity funds.

- Consistent treatment at group level: Investments qualifying for LTEI treatment at the individual insurer level are now consistently recognised in the calculation of group SCR, improving regulatory clarity.

The Attractiveness of LTEI-Eligible Private Equity for Insurers

The relaxation of Long-Term equity investment (LTEI) criteria under the Solvency II review is expected to improve the regulatory economics of private equity for European insurers.

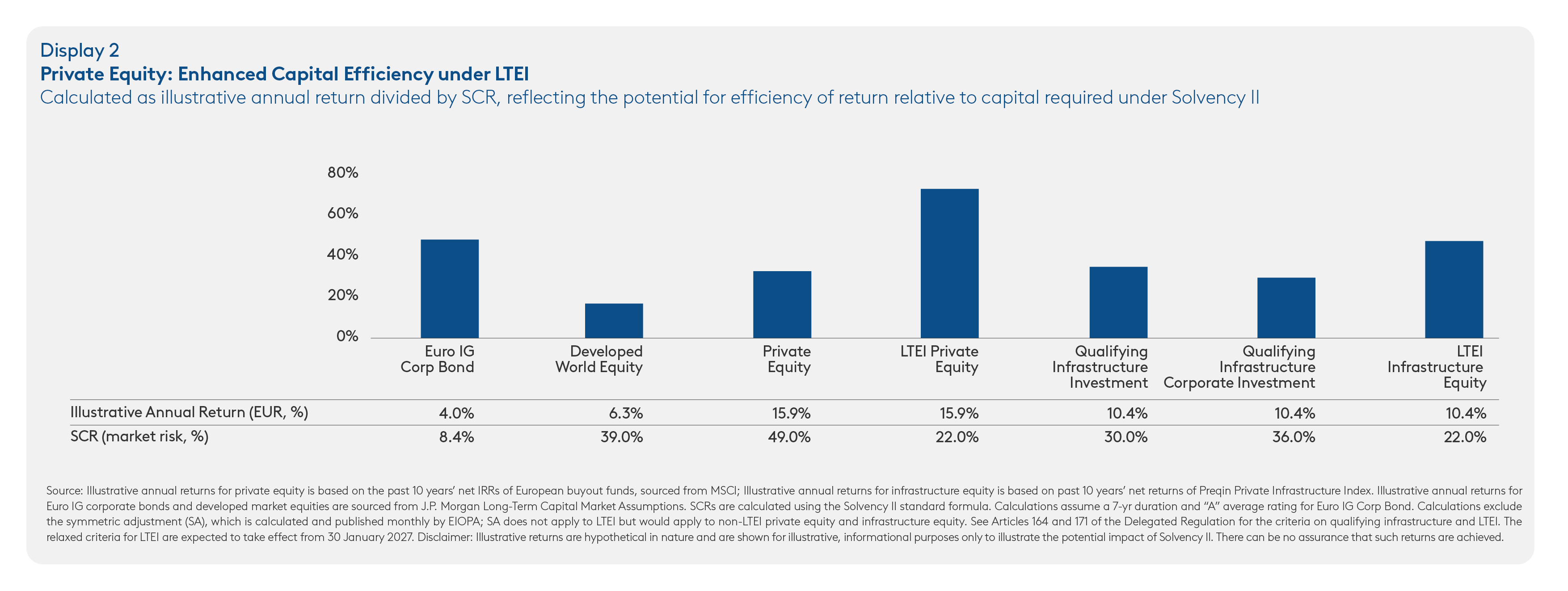

Display 2 compares capital efficiency – calculated as target annual return divided by Solvency II capital requirement (SCR) – across investment-grade fixed income, public equity, private equity, and infrastructure equity.

Under the revised LTEI framework, the SCR for eligible equity investments is reduced to 22%, enhancing the return-on-capital profile of private equity. As a result, private equity becomes a more capital-efficient asset class under Solvency II.

Infrastructure equity investments that qualify for LTEI treatment also benefit from the reduced capital requirement.7 While this represents a meaningful improvement, the impact is less pronounced than for private equity, given the lower baseline capital requirement. While LTEI may also apply to certain public equity investments, practical implementation is likely to be more limited given their liquid nature.

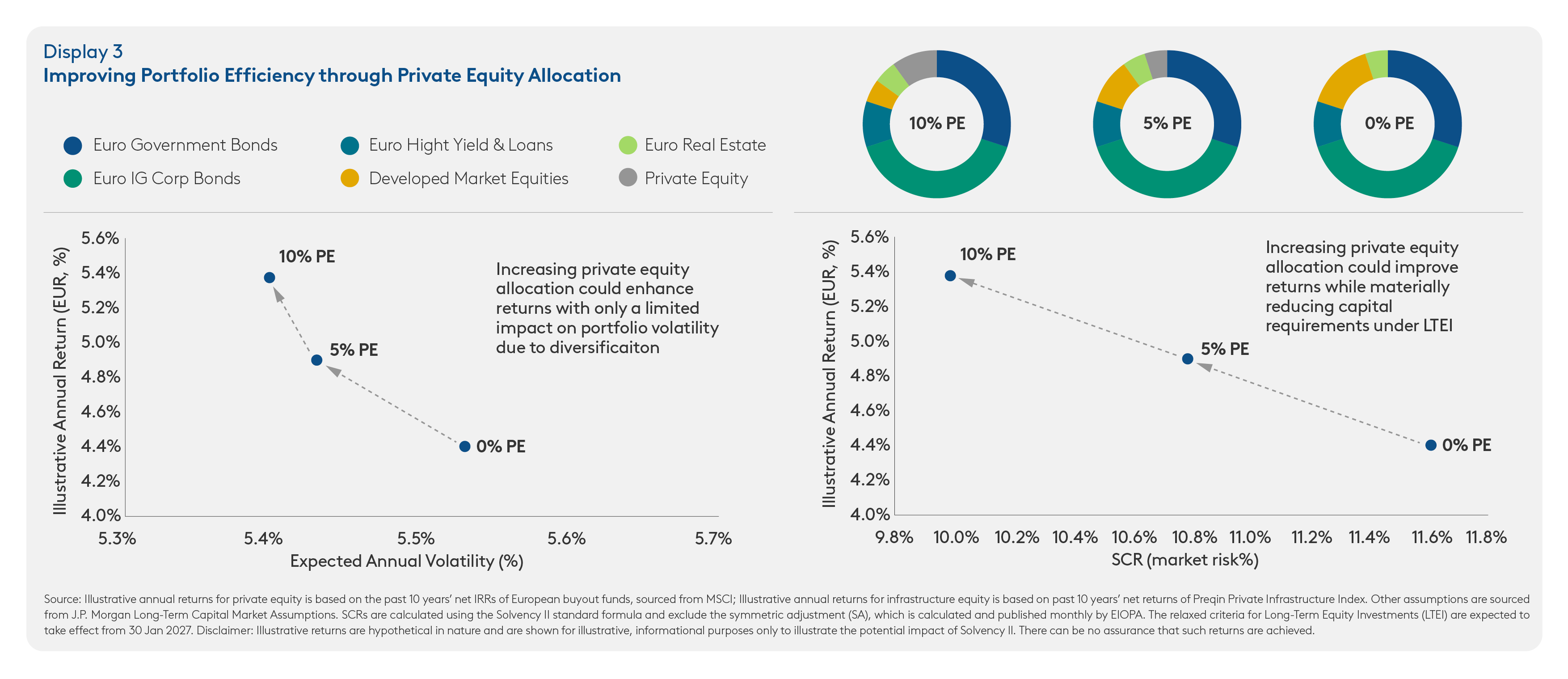

From a portfolio construction perspective, the LTEI framework has the potential to enhance the role of private equity within insurers’ strategic asset allocation.

As illustrated in Display 3, reallocating from public equities to LTEI-eligible private equity may improve both risk-adjusted returns and capital efficiency, representing a more efficient use of insurers’ risk and capital budgets. This reflects the ability to capture the illiquidity premium of private equity without a commensurate increase in regulatory capital requirements.

Furthermore, the LTEI capital requirement of 22% brings private equity closer to the capital treatment of long-duration corporate bonds. While private equity does not inherently provide duration, combining LTEI-eligible private equity with interest rate hedging strategies may offer a more capital-efficient approach to asset-liability management, compared to long-dated credit, particularly in a tightening spread environment. However, such strategies introduce liquidity risks: rising interest rates can trigger collateral calls on hedging positions and may force asset sales, making robust liquidity buffers and risk management essential.

Cross-jurisdiction capital treatment could be an important consideration for multinational insurers. LTEI-eligible private equity investments benefit from a 22% capital requirement, which is significantly lower than other regulatory regimes such as US RBC (~30%), Bermuda SCR (~45%), and Asia ICS (~49%). This disparity may provide European insurers with a structural advantage in allocating to private markets, enhancing their competitiveness in accessing long-term investment opportunities.

Implementation Considerations of LTEI

Private equity investments do not automatically qualify for LTEI. As such, insurers must undergo an eligibility assessment according to Solvency II Directive, Delegated Acts, EIOPA implementing technical standards, and national (local) regulations and supervisory practices.

In practice, private equity ELTIFs and unlevered AIFs managed by authorised EU AIFMs are more likely to meet the new LTEI criteria and benefit from the 22% capital requirement starting in January 2027, subject to insurers’ demonstration of “no forced sale.

To demonstrate compliance with the “no forced sale” requirement, insurers may adopt one of the following approaches to demonstrate their ability to avoid forced sales under both ongoing and stressed conditions:9

Approach 1:

- Life insurers: have sufficient illiquid liabilities with Macaulay duration > 9.5 years

- Non-life insurers: meet liquidity buffer threshold of 100%

Approach 2:

- Projected cash inflows exceed outflows under both base and stressed conditions over a 5-year horizon.

Conclusion

The Solvency II reform represents a structural inflection point for European insurers’ participation in private markets. By improving the capital efficiency of private equity and infrastructure equity, the revised LTEI framework creates a potentially compelling opportunity for insurers to increase allocations to long-term assets.

However, capital relief does not eliminate economic risk. Disciplined implementation, supported by robust governance, liquidity management, and ongoing supervisory engagement, remains critical.

Disclosure:

Nothing in this publication constitutes a valuation or investment judgment regarding any specific financial instrument, issuer, security, or sector mentioned or referenced herein. The content presented does not represent a formal or official view of CVC and is not intended to relate specifically to any investment strategy, vehicle, or product offered by CVC.

This publication is provided solely for informational purposes and is intended to serve as a conceptual framework to support investors in conducting their own analysis and forming their own views on the subject matter discussed.

No assurance can be given that any investment strategy discussed will be successful. Past market trends are not reliable indicators of future performance, and actual outcomes may vary significantly. The information, including any commentary on financial markets, is based on current market conditions, which are subject to change and may be superseded by subsequent events.

Performance data for any referenced indices is shown on a total return basis, with dividends reinvested. Such indices are unmanaged, do not include fees, expenses, or charges, and are not available for direct investment.

1 49% + Systematic Adjustment (SA) for unlisted equities. The SA is calculated and published by EIOPA on a monthly basis. Under the Solvency II Review, the bounds of the SA have been widened to a range of -13% to +13%, compared to -10% to +10% previously. The SA does not apply to the 22% SCR for LTEI. Please refer to Article 106 of Directive (EU) 2025/2 of the European Parliament and of the Council amending Directive 2009/138/EC

2 Commission Delegated Regulation (EU) 2026/269 of 29 October 2025 amending Delegated Regulation (EU) 2015/35 as regards technical provisions, long-term guarantee measures, own funds, equity risk, spread risk on securitisation positions, other standard formula capital requirements, reporting and disclosure, proportionality and group solvency.

3 20 days following the publication in the Official Journal of the European Union on 18th February 2026.

4 2024Q4 EIOPA Insurance Statistics, Asset Exposures.

5 Article 105a of Directive (EU) 2025/2 of the European Parliament and of the Council amending Directive 2009/138/EC; Article 169, 171, 336a of Commission Delegated Regulation (EU) 2026/269 amending Delegated Regulation (EU) 2015/35. Available at Official Journal of the European Union.

6 Article 171d of Commission Delegated Regulation (EU) 2026/269, available at Official Journal of the European Union.

7 LTEI-eligible infrastructure equity SCR: 22%; qualifying infrastructure investment SCR: 30% + 77%*SA; qualifying infrastructure corporate investment SCR: 36% + 92% * SA; non-LTEI, non-qualifying infrastructure equity SCR: 49% + SA

8 There can be no assurance that any CVC Fund will meet the LTEI Eligibility under Solvency II. Each insurer will need to conduct an assessment to determine eligibility.

9 Article 171 of Commission Delegated Regulation (EU) 2026/269, available at Official Journal of the European Union.